Intraday Momentum Signals This is an advanced divergence detection strategy designed to identify potential market reversals by analyzing the relationship between price action and momentum oscillator patterns. The strategy automatically detects divergence signals and executes trades based on configurable parameters.

⚠️ CRITICAL DISCLAIMER

READ THIS CAREFULLY BEFORE USING THIS STRATEGY:

This is NOT Financial Advice

❌ This is NOT a buy signal generator

❌ This is NOT a sell signal recommendation

❌ This is NOT investment advice

❌ This is NOT a guaranteed profit system

❌ This is NOT a substitute for professional financial guidance

Educational Purpose Only

✅ This tool is for educational and research purposes ONLY

✅ Provided for technical analysis learning

✅ Intended for strategy backtesting and study

✅ Use at your own risk and responsibility

Your Responsibility

🔍 DO YOUR OWN RESEARCH before making any trading decisions

🔍 VALIDATE all signals independently

🔍 BACKTEST thoroughly on historical data

🔍 PAPER TRADE before risking real capital

🔍 CONSULT a licensed financial advisor or SEBI-registered professional

🔍 UNDERSTAND the risks involved in trading

Risk Warning

⚠️ Trading involves substantial risk of loss

⚠️ You can lose your entire capital

⚠️ Past performance does NOT guarantee future results

⚠️ No strategy works 100% of the time

⚠️ Market conditions constantly change

⚠️ Never risk money you cannot afford to lose

Legal Notice

By using this strategy, you acknowledge that:

You are solely responsible for your trading decisions

The creator assumes no liability for your losses

You will not hold anyone responsible for outcomes

You understand this is not personalized advice

You agree to trade at your own discretion and risk

🎯 Best Use Cases

This strategy is primarily designed for intraday trading and works optimally on shorter timeframes:

Recommended Timeframes

✅ 3-minute charts - Ultra-short scalping (High risk, requires constant monitoring)

✅ 5-minute charts - MOST RECOMMENDED for intraday

✅ 15-minute charts - Balanced intraday approach

✅ 30-minute charts - Swing intraday positions

⚠️ 1-hour charts - Fewer signals but potentially higher quality

NOT Recommended For

❌ Daily or weekly timeframes

❌ Long-term investing

❌ Position trading

❌ Swing trading (multi-day holds)

Why Intraday? The divergence detection logic is specifically optimized for intraday price movements and momentum oscillations that occur within a single trading session.

🔧 Core Features

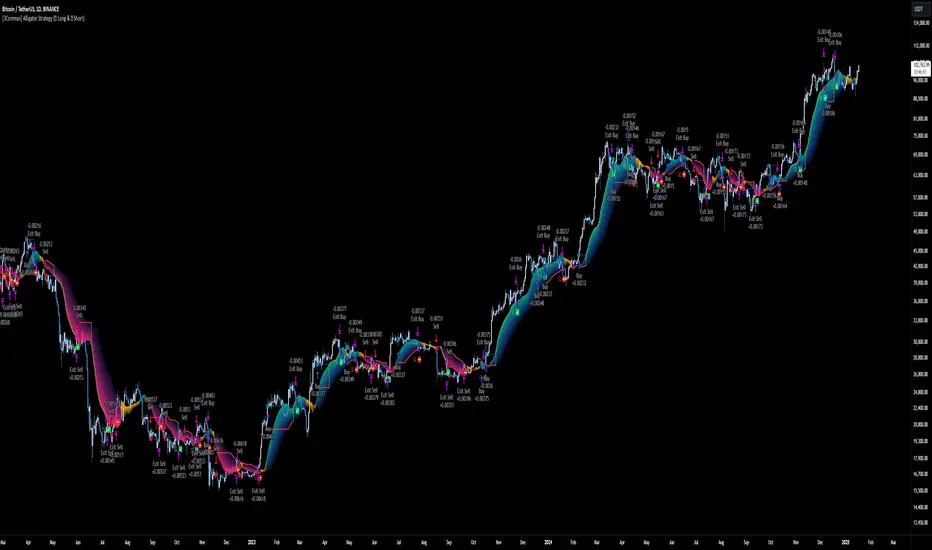

1. Divergence Detection Engine

The strategy identifies four types of divergence patterns:

Regular Bullish (UP) - Price makes lower lows while oscillator makes higher lows (potential reversal up)

Hidden Bullish (L+) - Price makes higher lows while oscillator makes lower lows (trend continuation)

Regular Bearish (DN) - Price makes higher highs while oscillator makes lower highs (potential reversal down)

Hidden Bearish (S+) - Price makes lower highs while oscillator makes higher highs (trend continuation)

2. Configurable Parameters

Oscillator Settings:

Period Length (default: 9) - Controls sensitivity

Source (default: close price) - Can use OHLC

Lookback Right/Left - Pivot detection sensitivity

Lookback Range (5-60) - Time window for divergence comparison

Exit Strategy:

Take Profit Level (default: 80) - Oscillator level for profit booking

Stop Loss Options: ATR-based, Percentage-based, or None

Trailing Stop Loss - Dynamic risk management

Visual Controls:

Toggle each divergence type on/off

Customizable dashboard position (4 corners)

Clear visual signals on oscillator panel

3. Risk Management System

The strategy includes three stop-loss mechanisms:

A) ATR Trailing Stop (Recommended for volatile markets)

Dynamically adjusts based on market volatility

Uses Average True Range multiplier

Trails as position moves in profit

B) Percentage Stop (Fixed risk)

Set percentage from entry price

Simple and predictable

Good for consistent position sizing

C) Manual Exit (Signal-based only)

Exits on oscillator threshold

Exits on counter-divergence signal

No automatic stop loss

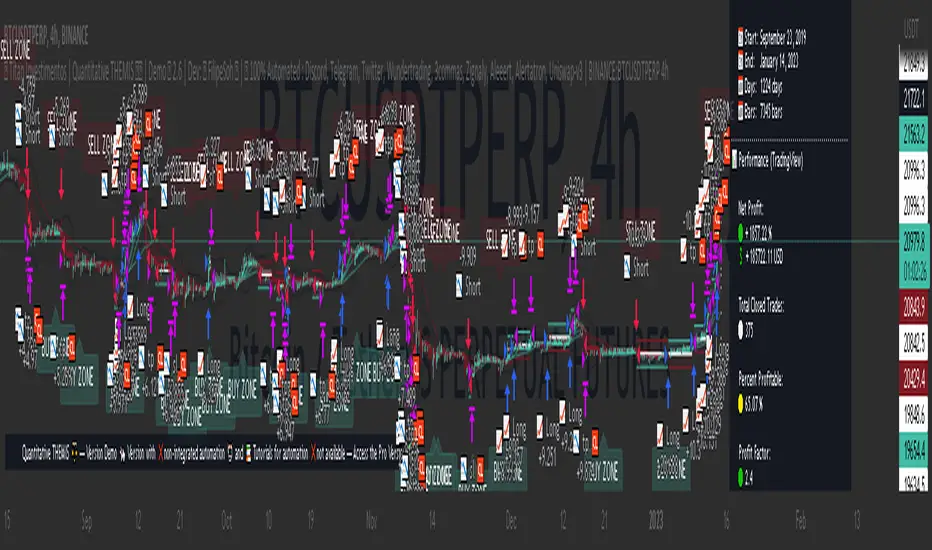

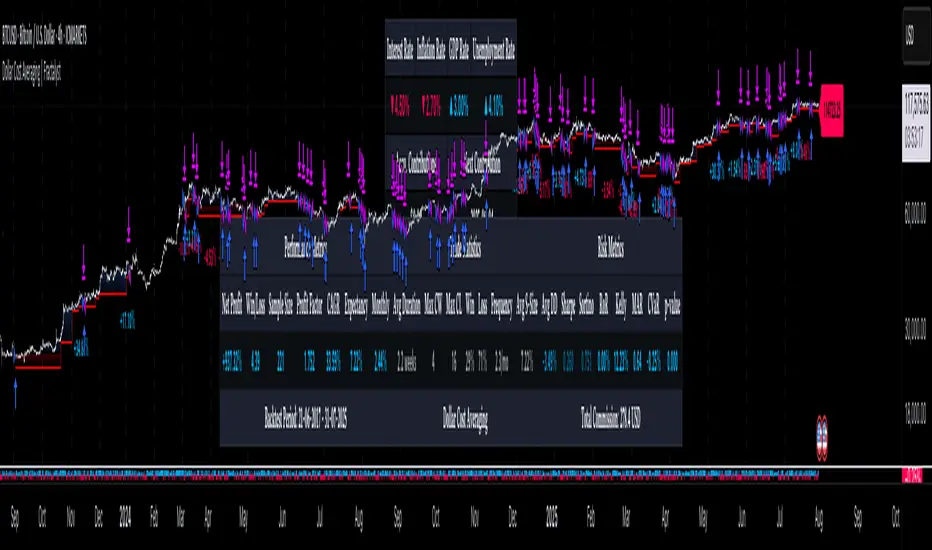

4. Performance Dashboard

Real-time comprehensive statistics:

MetricDescriptionTotal TradesNumber of completed tradesWin RatePercentage of profitable tradesWinning TradesCount of profitable positionsLosing TradesCount of loss-making positionsNet ProfitTotal profit/loss in currencyProfit FactorGross profit ÷ Gross lossAvg WinAverage winning trade amountAvg LossAverage losing trade amountLargest WinBest single trade profitLargest LossWorst single trade loss

Color Coding:

🟢 Green - Positive/Good metrics (Win rate >60%, PF >2)

🟠 Orange - Neutral metrics (Win rate 50-60%, PF 1-2)

🔴 Red - Negative/Poor metrics (Win rate <50%, PF <1)

📈 How The Strategy Works

Signal Generation Process

Continuous Monitoring

Strategy scans every bar for pivot points

Compares current pivot with historical pivots

Checks for divergence between price and oscillator

Entry Trigger

Valid divergence pattern detected

Lookback range conditions met

Automatic long position opened

Entry price and stops calculated

Position Management

Selected stop-loss mechanism activated

Trailing stop updates on each bar (if enabled)

Take-profit level monitored

Exit Execution

Oscillator crosses take-profit threshold, OR

Opposite divergence signal appears, OR

Stop-loss triggered

Performance Logging

Trade recorded in statistics

Dashboard updated in real-time

Profit/loss calculated and displayed

⚙️ Recommended Settings for Intraday

🕐 For 3-Minute Charts (Scalping)

Period: 9-12

Lookback Range: 5-40 bars

Take Profit Level: 80-85

Stop Loss: 2-3% OR ATR (14, 2.5x)

Use Case: Rapid entries/exits, high frequency, requires constant attention

🕔 For 5-Minute Charts (MOST POPULAR)

Period: 9-14

Lookback Range: 5-60 bars

Take Profit Level: 75-80

Stop Loss: 3-5% OR ATR (14, 3.5x)

Use Case: Balanced risk/reward, good signal frequency, manageable monitoring

🕒 For 15-Minute Charts (Swing Intraday)

Period: 9-14

Lookback Range: 5-60 bars

Take Profit Level: 70-80

Stop Loss: 4-6% OR ATR (14, 3.5x)

Use Case: Fewer but higher quality signals, less screen time

🕧 For 30-Minute Charts

Period: 12-14

Lookback Range: 5-60 bars

Take Profit Level: 70-75

Stop Loss: 5-7% OR ATR (14, 4.0x)

Use Case: Extended intraday positions, better for part-time traders

📝 Important Usage Notes

Strategy Configuration

✅ Works in both indicator and strategy modes

✅ Pyramiding: Up to 2 concurrent positions allowed

✅ Default capital: ₹100,000 (customizable)

✅ Fixed quantity: 2 units per trade (customizable)

✅ Currency: INR (can be changed)

Visual Signals

Visual divergence signals plotted on oscillator panel (not price chart)

Entry/exit labels show profit/loss for each closed trade

Lines and shapes clearly mark divergence points

Dashboard provides at-a-glance performance overview

Limitations

⚠️ Divergences are lagging by nature (require confirmed pivots)

⚠️ Not all divergences result in reversals

⚠️ False signals increase in choppy/ranging markets

⚠️ Requires minimum volatility to function properly

⚠️ Performance degrades in strong trending markets (for counter-trend setups)

🎨 Visual Elements Explained

Oscillator Panel

Blue solid line - Main momentum oscillator (0-100 range)

Dotted line at 70 - Overbought threshold

Dotted line at 30 - Oversold threshold

Dotted line at 50 - Centerline (bullish above, bearish below)

Shaded background - Visual reference zone

Divergence Markers

Blue solid dots/lines - Regular bullish divergence

Light blue dots/lines - Hidden bullish divergence

Red solid dots/lines - Regular bearish divergence

Orange dots/lines - Hidden bearish divergence

Labels

"UP" label - Long entry on regular bullish divergence

"L+" label - Long entry on hidden bullish divergence

"DN" label - Potential exit/reversal (bearish divergence)

"S+" label - Potential exit/reversal (hidden bearish)

⚡ Performance Optimization Tips

Before Going Live

Backtest Extensively

Test on at least 6-12 months of historical data

Use different market conditions (trending, ranging, volatile)

Check performance across multiple instruments

Paper Trade First

Practice on demo account for minimum 1 month

Validate signals manually before trusting automation

Understand why trades win or lose

Optimize Parameters

Adjust lookback ranges for your specific market

Fine-tune take-profit levels based on average moves

Test different stop-loss methods

Monitor win rate - aim for >50% minimum

Risk Management

Never risk more than 1-2% of capital per trade

Use position sizing based on stop distance

Set maximum daily loss limits

Keep a trading journal

During Live Trading

✅ Monitor market conditions (trending vs ranging)

✅ Avoid trading during major news events

✅ Respect your stop losses - never remove them

✅ Take partial profits if trade moves significantly

✅ Review and adapt based on actual performance

Red Flags to Watch

🚩 Win rate suddenly drops below 40%

🚩 Profit factor falls below 1.0

🚩 Average loss exceeds average win

🚩 Consecutive losing streak (5+ trades)

🚩 Strategy stops generating signals

If you see these signs: Stop trading, re-evaluate parameters, check market conditions, or consider if market character has changed.

🔬 Research & Development Suggestions

Since you must DO YOUR OWN RESEARCH, here are areas to explore:

Parameter Optimization

Test different oscillator periods for your instrument

Experiment with lookback ranges

Find optimal take-profit levels through data analysis

Compare ATR vs percentage stops

Market Selection

Which stocks/indices show best results?

Does it work better in certain sectors?

Intraday vs specific session times (opening, closing)

Combination Strategies

Add volume filters

Combine with trend indicators

Use support/resistance confirmation

Add fundamental filters for stock selection

Risk Improvements

Implement time-based exits (close before market close)

Add volatility filters

Create different parameter sets for different market conditions

📚 Educational Resources

To properly understand and research this strategy:

Study divergence trading concepts thoroughly

Learn about momentum oscillators and their behavior

Understand pivot points and how they form

Research market psychology behind reversals

Learn proper position sizing and risk management

Study technical analysis fundamentals

Recommended Learning Path:

Technical Analysis basics

Oscillator indicators deep dive

Divergence patterns and their reliability

Backtesting methodologies

Risk and money management

Trading psychology

✋ Final Reminder

BEFORE YOU CLICK "BUY" OR "SELL":

✅ Have you backtested this thoroughly?

✅ Have you paper traded for at least 1 month?

✅ Do you understand WHY each signal triggers?

✅ Have you calculated your position size properly?

✅ Have you set your stop loss?

✅ Can you afford to lose this money completely?

✅ Have you consulted a financial professional?

✅ Are you trading with a clear, calm mind?

If you answered NO to any of these - DO NOT TRADE YET.

📞 Support & Responsibility

This strategy code is provided "as-is"

No warranty or guarantee of any kind

User assumes all responsibility and risk

Past results do not predict future performance

Creator is not liable for any trading losses

Trading is risky. Most traders lose money. Trade responsibly or not at all.

Strategia Pine Script®